Platinum – Supply and Demand

Platinum – Part 2 of a 2-Part Presentation

Platinum price to rise as “climate change” pressure gains traction

Supply and demand

Supply

The global supply of platinum (and PGMs) depends heavily on the South African PGM industry. South Africa supplies some 73%, 37% and 82% of global platinum, palladium and rhodium respectively. South Africa produces c.4.5moz of the c.6.1moz of global production (JM).

The market is of the view that there is an increasing risk of a decline in supply from South African PGM mines as shafts/mines are reaching the end of their life and/or have become economically unviable.

In addition, the industry has faced numerous challenges in the past caused mainly by the combined effects of prolonged industrial action and electricity shortages, increasing costs, a significant reduction in capital expenditure, and a negative legal and political environment (Section 54, Mining Charter). The industry is currently experiencing daily and prolonged electricity outages, which has a negative impact on the primary supply of PGMs.

I am of the view that these risks, particularly electricity outages, will not abate for at least five years. Under these circumstances, the risk to the supply of PGMs from South African mines is to the downside. In this regard, the negative impact on supply will put upward pressure on PGM prices (repeating past experience).

Demand

In this review, I have discussed those factors that in my view, will likely accelerate PGM demand and in particular the demand for platinum. In summary, and for clarity, I reiterate my view that the demand for PGMs has been and will continue to be driven by progressively tighter vehicle standards through regulation worldwide. In response, vehicle manufacturers have had to increase the content (loading and loading ratios) of palladium, platinum and rhodium (PGMs) in autocatalysts to meet the stricter limits, thereby progressively increasing demand. Vehicle manufacturers have shifted significantly to the introduction of electrification, hybrids and FCEVs in an attempt to comply with tighter emission standards.

The increase in demand for platinum was, however, constrained “twice” during the intervening period. Firstly, by the substitution of platinum for palladium in petrol autocatalysts and partial substitution of platinum with palladium in diesel autocatalysts. Secondly, by Dieselgate, which resulted in a loss of diesel market share from 2016, which, in turn, had an impact on platinum demand. In this regard, autocatalyst demand declined by -2.3% (CAGR) between 2007 and 2019f (JM). In comparison, palladium autocatalyst demand increased by 6.7% (CAGR) over the same period.

The onset of regulation surrounding greenhouse gases (CO₂) will likely accelerate PGM demand, particularly for platinum. Hybrid diesel vehicles, which contain platinum as the primary metal in their autocatalysts, emit less CO₂ and are more fuel efficient than petrol hybrid vehicles. Furthermore, hybrid vehicles, petrol and diesel, require additional loadings of palladium and platinum.

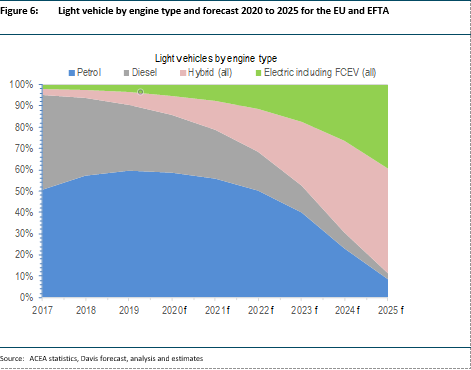

In my view, it is inevitable that petrol and diesel internal combustion engines (ICEs) will likely be phased out faster than generally expected and will be replaced by BEVs and FCEVs and a combination of hybrid vehicles. Figure 6 illustrates my forecast of the “phasing out” of ICE vehicles and the “phasing in” of BEVs, FCEVs and a combination of hybrid vehicles (EU and EFTA).

I am of the opinion that it is important to gain a “sense” of the quantum of the possible annual increase in platinum autocatalyst demand by 2025. It should be noted that this demand is likely to increase exponentially as ICE vehicles fall away and hybrid, BEVs and FCEVs gain market share.

Stepping into the “minefield” of “simple forecasting” my calculations indicate that by 2022 and 2025 additional platinum demand of around c.300koz and c.1.0moz respectively will be required. These figures were calculated at a high rate of decline of ICE vehicles. It should be noted that these figures only give a “sense” of the quantum for the exponential acceleration of platinum demand.

Market balance

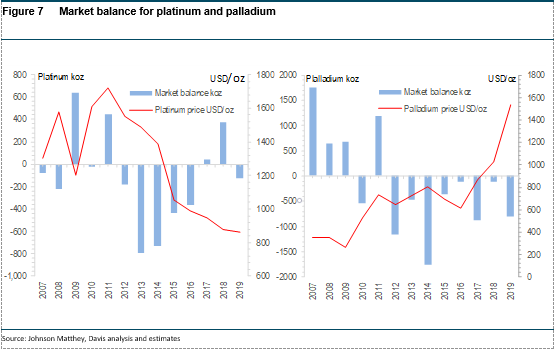

The supply-and-demand fundamentals for platinum are difficult to unpack when compared to the supply-and-demand fundamentals for palladium. Figure 7 illustrates the market balance for platinum and palladium respectively (JM). On the macro long-term level, platinum has exhibited an average annual net market balance deficit of some c.110koz and a total deficit of some c.1.45moz between 2007 and 2019 respectively (JM data). Significant deficits are noted between 2013 and 2016. In 2013, the market deficit increased to around c.800koz, mainly due to an increase in investment and gross platinum demand. In 2014, a deficit of around c.700koz was recorded due mainly to a loss in supply of over c.1.3moz of platinum production following a five-month strike at major South African mines. In 2015, the market deficit decreased to around c.400koz, mainly due to growth in autocatalyst and investment demand. As indicated above, Dieselgate precipitated a backlash against diesel resulting in a loss of diesel market share, which, in turn, had an impact on platinum demand.

I note, that both platinum and palladium have reflected annual deficits, which suggests both metals are exhibiting supply imbalances, yet the price of palladium has sky-rocketed and the price of platinum has been in free fall. Plainly, this situation is incongruent and flies against all financial norms. Financial markets are unlikely to misprice these metals ceteris paribus. I attribute much of this phenomenon to negative market sentiment towards platinum, given its history. It is interesting to note, that JM had a similar view: reporting that “the platinum market suffered from negative sentiment and falling prices in 2015, but demand trends were broadly positive”.

It is apparent, from research that the majority of the platinum market balance deficits illustrated in Figure 5 have a large component of investment demand, which has acted as a swing factor in the market balance calculation. I am of the view that this situation will likely change with the accelerated introduction of FCEVs and hybrid vehicles. In this regard, I expect the platinum market balance to go into deficit by 2022/2023 without the aid of investment demand.

I note that Sibanye-Stillwater anticipates a market balance surplus until 2022 and thereafter to revert to a continuous deficit which becomes considerable from 2025.

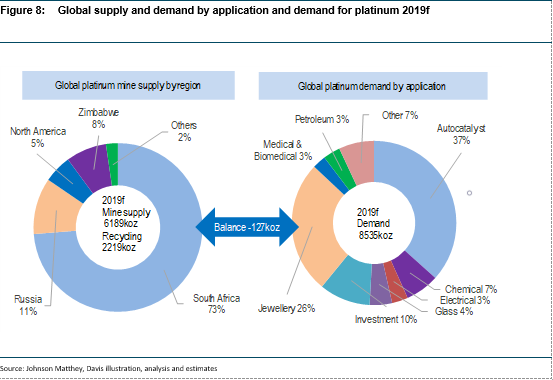

As indicated above, the supply-and-demand fundamentals for platinum are difficult to unpack and present. Most market research organisations present a complicated table of supply and demand, which results in a market balance figure at the bottom of the table. Figure 8 below illustrates a simple and unique presentation of supply and demand using JM statistics for 2019F. This presentation allows the reader to visualise the components and quantum of the supply-and-demand equation and readily understand how the market balance is calculated.

What do these trends imply and how they will impact the price of platinum

Throughout this discussion, I have alluded to a number of factors that will put upward pressure on the price of platinum. This upward movement in the price will likely be supported by the combination of a number of market indicators characterised by strong consumer demand and tight physical availability, coupled with a continuous supply and demand market balance deficit after 2022, which accelerates from 2025. The price is, however, likely to trend upwards, with some volatility, prior to 2022.

In my view the platinum price is primed for better days:

- The primary supply from South Africa is in decline.

- The continuity of South African production is not secure: currently, there are power outages in South Africa. These power outages are likely to be in place for at least five years and will have an impact on platinum production. The risk is to the downside.

- The demand for platinum will accelerate “significantly” within the next five years as global environmental “climate change” pressures gain traction combined with ever tightening vehicle tailpipe emission standards. Vehicle manufacturers have had to increase the content (loading and loading ratios) of palladium, platinum and rhodium (PGMs) in autocatalysts to meet the stricter limits.

- The significance of the reduction of the platinum content in fuel cells cannot be overestimated as this step change opens the door for platinum demand to accelerate.

- It is inevitable that petrol and diesel internal combustion engines (ICE) will be phased out faster than generally accepted and will be replaced by BE vehicles and FCEVs and a combination of hybrid vehicles. Hybrid diesel requires an increase in autocatalyst platinum loading.

- I am of the view that the market share of FCEVs will increase more rapidly than generally accepted and be of similar growth to that of hybrid and BE vehicles. Note that the growth between 2018 and 2019 was around c. 48% for hybrid and BE vehicles.

- The palladium price premium over platinum has increased significantly to around

c. USD1360/oz (10 February 2020). Under these circumstances, the substitution of palladium for platinum in petrol applications is on the cards. Substitution may well happen in as little as two years. This development will be positive for platinum demand. - Investment demand was renewed substantially, by around c. 900koz, in 2019. This increase in demand implies that investors are beginning to factor in low prices and positive fundamental outlook for platinum.

About Dr David Davis PhD. MSc. MBL. CEng. CChem. FIMMM. FSAIMM. FRIC.

David has been associated with the South African mining industry and mining investment industry for the past 43 years (mainly PGM, gold and uranium). At present, David is working as an independent precious metal consultant. David’s PhD involved: “Studies in the catalytic reduction and decomposition of nitric oxide 1976”.

Important Notice

General Disclosures, Disclaimers and Warnings

This Report (“the report”) in respect of the global Rhodium Industry is directed at and is being issued on a strictly private and confidential basis to, and only to, Professional Clients and Eligible Counterparties (“Relevant Persons”) as defined under the Investment Research Regulatory Rules and is not directed at Retail Clients. This report must not be acted on or relied on by persons who are not Relevant Persons. Any investment or investment activity to which this Report relates is available only to Relevant Persons and will be engaged in only with Relevant Persons.

The Report does not constitute or form part of any invitation or offer for sale or subscription or any solicitation for any offer to buy or subscribe for any securities in any Company discussed nor shall it or any part of it form the basis of or be relied upon in connection with any contract or commitment whatsoever.

The opinions, estimates (and where included) projections, forecasts and expectations in this report are entirely those of Dr David Davis as at the time of the publication of this report, and are given as part of his normal research activity, and should not be relied upon as having been authorised or approved by any other person, and are subject to change without notice. There can be no assurance that future results or events will be consistent with such opinions, estimates (where included) projections, forecasts and expectations. No reliance may be placed for any purpose whatsoever on the information or opinions contained in this Report or on its completeness and no liability whatsoever is accepted for any loss howsoever arising from any use of this Report or its contents or otherwise in connection therewith. Accordingly, neither Dr David Davis nor any person connected to him, nor any of his respective Consultants make any representations or warranty in respect of the contents of the Report. Prospective investors are encouraged to obtain separate and independent verification of information and opinions contained in the Report as part of their own due diligence. The value of securities and the income from them may fluctuate. It should be remembered that past performance is not necessarily a guide to future performance.

Dr David Davis has produced this report independently of the companies that may be named in this report except for verification of factual elements. Any opinions, forecasts, projections, or estimates or other forward-looking information or any expectations in this Report constitute the independent judgement or view of Dr David Davis who has produced this report (independent of any company discussed or mentioned in the Report or any member of its group).

The Report is being supplied to you for your own information and may not be reproduced, further distributed to any other person or published, in whole or in part, for any purpose whatsoever, including (but not limited to) the press and the media. The distribution of the Report in certain jurisdictions may be restricted by law and therefore any person into whose possession it comes should inform themselves about and observe any such restriction.

The Report has been prepared with all reasonable care and is not knowingly misleading in whole or in part. The information herein is obtained from sources that Dr David Davis considers to be reliable but its accuracy and completeness cannot be guaranteed.

Dr David Davis Certification

Dr David Davis attests that the views expressed in this report accurately reflect his personal views about the global Platinum Industry. Dr David Davis does not hold any interest or trading positions in any of the Companies mentioned in the report.