Markets Brace For Middle East Escalation

Over the last three weeks, many questions have been asked about why the US was maneuvering military assets into the Eastern Mediterranean and across allied Gulf states.

Those questions were answered on Saturday.

At around 2am New York time (5pm Sydney time) the US and Israel launched a widespread combat operation in Iran targeting military positions as well as political leadership sites.

Simmering geopolitical tensions have been one of the pillars of support for precious metals prices over the last several years.

Typically, Gold, Silver and Platinum will attract a stronger safe haven bid once the political tensions deteriorate into a kinetic military response.

Incoming data, including battle damage assessments, will be key factors in determining how much of last week’s rally could be extended higher over the short-term.

For the week, physical Gold priced in USD hit a one-month high of $5280.00 and finished the week with a 3.3% gain at $5278.00

Gold denominated in AUD posted a solid 2.9% gain for the week and settled at $7409.00.

If the conflict in Iran destabilizes a broader area of the Middle East early in the week, upside targets in USD and AUD Gold could reach $5450.00 and $7600.00, respectively.

Physical Silver posted its first weekly close above its 30-Day Moving Average (30-DMA) since the 4th of February. This was good enough for a 10.8% weekly gain and a close at $93.76.

The next key resistance level is $103.70.

Silver denominated in AUD posted its first weekly close above its 30-DMA since January 29th and finished the week with a 10.5% gain at $131.45. Key upside resistance is at $140.60.

The Gold versus Silver ratio moved 6.5% lower in favor of Silver and closed at 56.10. That means it takes 56.10 ounces of Silver to equal the price of one ounce of Gold.

Physical Platinum had its strongest week of the year with a 10.8% gain to close at $2365.00. The break above $2335 negates the Flag pattern and now points to the $2460/80 range.

As mentioned above, geopolitical tension is one of the pillars of support for the precious metals complex.

Other pillars are: rising global debt levels, persistent fiscal deficits and renewed trade tensions, which continue to reinforce the strategic appeal for Gold, Silver and Platinum.

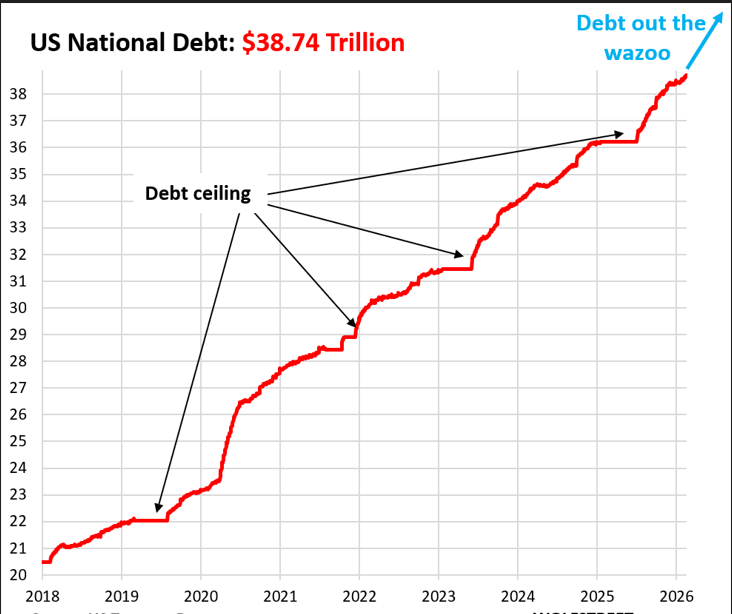

At the end of Q4, the US national debt reached $38.51 trillion, having soared by yet another $2.30 trillion over the 12 months in the calendar year 2025, or by 6.3%.

This includes the first half of the year, when the debt ceiling blocked the government from adding to its mountain of Treasury securities, and the level of debt got stuck for six months.

And then in July, after the debt ceiling was resolved, the debt began to explode. All of that $2.3 trillion was added in the second half amid a tsunami of debt issuance.

In Q4 2025 alone the debt rose by $877 billion, or by 2.3% from Q3.

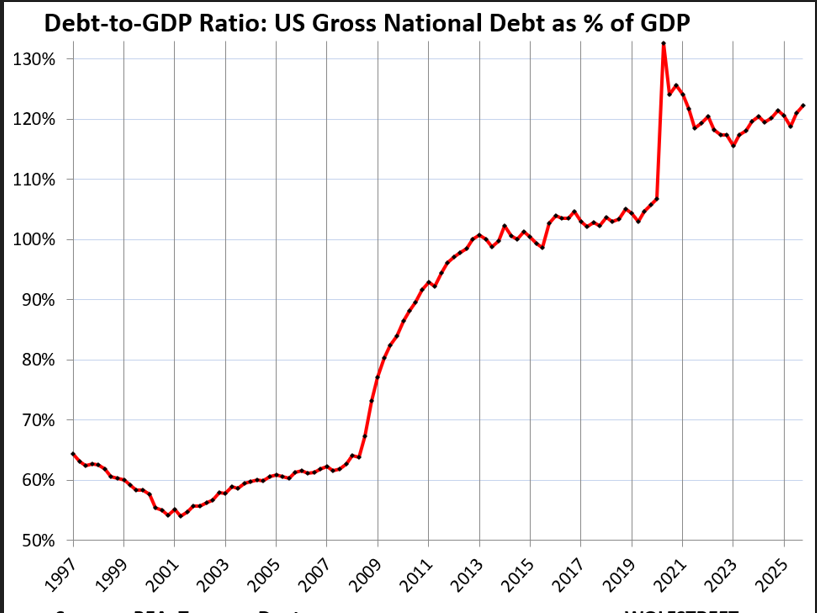

As illustrated on Chart 1, the US debt-to-GDP ratio rose to 122.3% at the end of Q4, the highest since Q1 2021, as the COVID spike was winding down.

This debt is the actual amount in Treasury securities that the US government owes and cannot walk away from.

They are either traded in the markets ($28.84 trillion) or are held by government pension funds, the Social Security Trust Fund, etc.

For the whole year, the debt increased by 6.3%, and the current USD GDP increased by 5.6%.

The debt-to-GDP ratio is important because an economy generates tax revenues that grow roughly with the economy, and tax revenues are needed to service this debt.

If the economy grows faster than the debt year after year, then the burden of that debt on the economy begins to lessen. But that’s not happening at this point.

For now, as shown on Chart 2, this growing debt-to-GDP ratio means a more leveraged government, and a higher burden on the economy, which has spiked by 88% in seven years, to $38.74 trillion as of last week.

With this mind, the precious metals complex remains supported by a simple reality: uncertainty is abundant, debt continues to climb, and policymakers are navigating an increasingly complex and hostile geopolitical landscape in real time.

In this environment, investors with a longer-term perspective are adding to precious metals positions on dips.

In short, the debate is no longer whether Gold, Silver and Platinum deserve a place in a conservative portfolio.

The real question is how much wealth security via hard assets is enough when the world is as unpredictable as it is today?

Judging by last week’s price action, many investors would rather hold a little extra of the safe haven assets just in case the world delivers another surprise down the road.

Now is the time to consider making Gold, Silver and Platinum the secure cornerstone assets in your long-term wealth creation strategy.

This publication has been prepared for the GBA Group Companies. It is for education purposes only and should not be considered either general of personal advice. It does not consider any particular person’s investment objectives, financial situation, or needs. Accordingly, no recommendation (expressed or implied) or other information contained in this report should be acted upon without the appropriateness of that information having regard to those factors. You should assess whether or not the information contained herein is appropriate to your individual financial circumstances and goals before making an investment decision or seek the help the of a licensed financial adviser. Performance is historical; performance may vary; past performance is not necessarily indicative of future performance. Any prices, quotes or statistics included have been obtained from sources deemed to be reliable, but we do not guarantee their accuracy or completeness.