FOMC Minutes Signal Rising Stagflation Fears

by Joel Cameron

Posted on 13 Jul, 2026 in

As Summertime in the Northern Hemisphere moves into full swing, it’s not surprising to see financial markets contained within recent ranges.

Based on last week’s price action, it seems the precious metals complex is more concerned about the trajectory of US interest rates than the ever-precarious conflict in the Persian Gulf.

Last Wednesday’s release of the FOMC minutes was perceived as foreshadowing a FED FUNDS hike within a few months, which bumped Treasury yields higher and capped Gold, Silver and Platinum prices.

Physical Gold priced in USD traded in a relatively narrow $180.00 range from top to bottom and finished the week 1.3% lower at $4118.00.

Technical indicators are largely neutral with the Relative Strength Index (RSI) at 44.40.

The 30-Day Moving Average (30-DMA) is at $4197.00 with initial support in the $4060 to $4070.00 range.

Gold denominated in AUD slipped 1.6% lower for the week and closed at $5920.00. We see initial support near $5830.00 and a close above $5990.00 would improve the technical outlook.

Physical Silver priced in USD traded in a $4.00 range for the week and settled 4.1% lower at $59.80.

Momentum indicators are not flashing any strong directional signals, with the daily RSI at 40.00. Initial support is $57.75, and a close above $64.50 would suggest a durable low is in place.

Silver denominated in AUD fell 4.3% and finished the week at $85.95. The 30-DMA looks out of range this week at $92.10, and initial support is in the $83.40 to $83.60 range.

The Gold versus Silver ratio closed 2.8% higher in favor of Gold at 68.70. This means it takes 68.70 ounces of Silver to equal the price of one ounce of Gold.

Physical Platinum prices were contained in a $95.00 range from top to bottom for the week and finished fractionally lower at $1631.00.

The daily technical picture is becoming increasingly more bullish with the RSI at 44.50 and rising and the 30-DMA within reach at $1695.00

Even though the FOMC voted unanimously to hold interest rates unchanged at their June 17th meeting, last week’s minutes reflected a wide range of opinions about the central bank’s monetary policy direction.

However, the three aspects of the US economy that all voting members agreed upon were: consumer inflation is too high, and employment and GDP growth are too low.

The textbook definition of these concurrent economic conditions is Stagflation, which is generally positive for hard assets.

Stagflation is when an economy experiences stagnant employment growth, stagnant growth in GDP, and above target consumer inflation.

In this type of economic environment, the central bank is usually very reluctant to lift its key interest rate to tackle the inflation problem.

Why do central banks avoid raising rates during a period of Stagflation?

Because raising rates can tip the economy into a contraction of growth and possibly a recession.

A recession is a period of negative economic activity, as measured by GDP, for at least two quarters in a row.

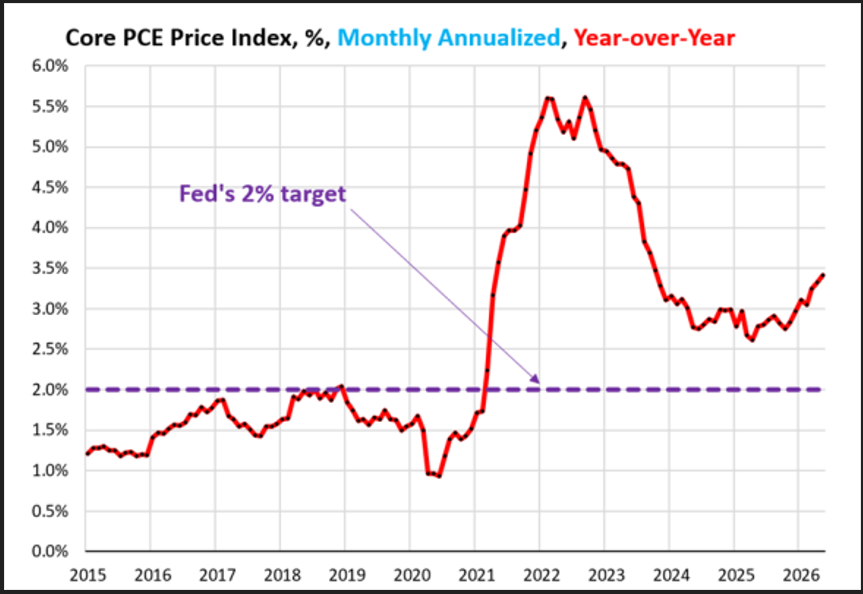

As illustrated on Chart 1, The annual Personal Consumption Expenditures (PCE) inflation rate in the US jumped to 3.3% in March 2026, marking the highest level since May 2024 and well above the FED’s target of 2.00%.

Figures came in line with forecasts, with the rise primarily driven by higher energy costs (12.5%), mostly gasoline (up 18.9%) and fuel oil (44.2%), due to the conflict in the Persian Gulf.

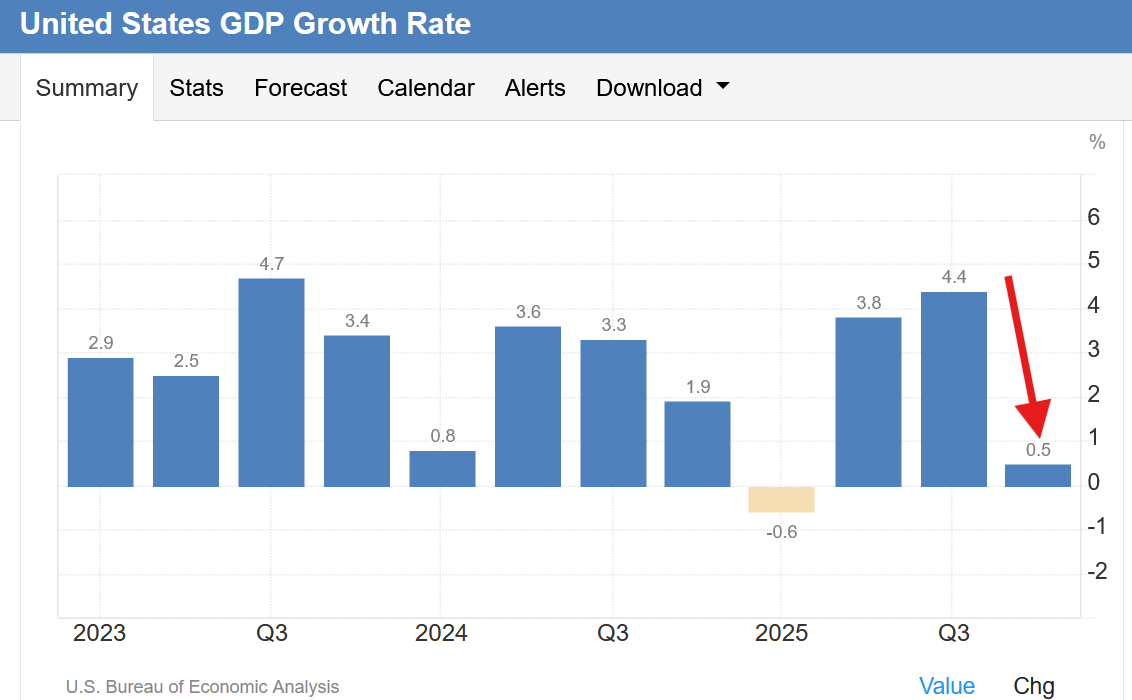

As shown on Chart 2, US GDP growth has stalled over the last three months on just the perception of higher FED Funds rates going into the second half of the year.

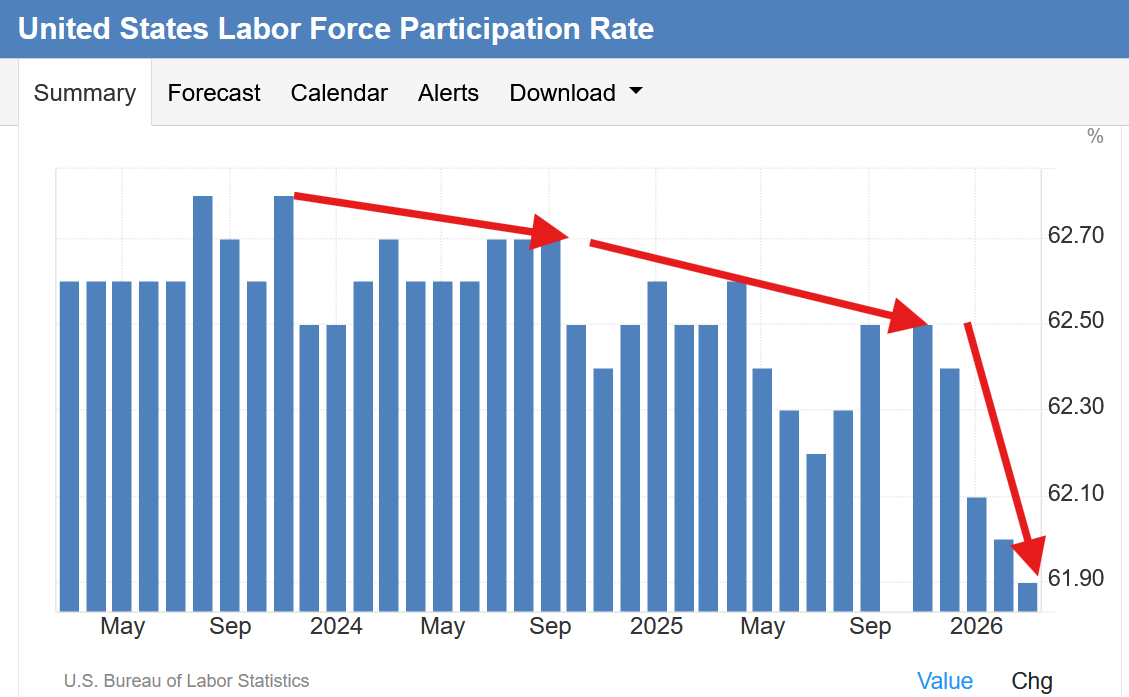

And, as shown on Chart 3, as the US GDP has dropped, the US Labor Force Participation rate has also suffered a sharp contraction.

On balance, these three charts simplify the argument of why the FED can talk about raising rates, and maybe even raise the FED Funds target once.

But the probability that the FED can start a protracted tightening cycle in this Stagflationary economic environment seems very low.

Further, Stagflation is not just an American problem.

Several nations in the EU, Asia, as well as developing economies are experiencing low GDP growth rates combined with high debt levels and sticky inflation.

Which is an integral reason why central banks are on pace to buy over 1000 tons of Gold this year.

Precious metals prices tend to rise handsomely during periods of Stagflation.

That is because hard assets are a time-proof store of value that offer wealth security for investors of all levels of sophistication.

With the precious metals currently rangebound and off the boil, now is the time to consider divesting from some paper assets and adding to your holdings of physical Gold, Silver and Platinum before the next leg higher.

This publication has been prepared for the GBA Group Companies. It is for education purposes only and should not be considered either general of personal advice. It does not consider any particular person’s investment objectives, financial situation, or needs. Accordingly, no recommendation (expressed or implied) or other information contained in this report should be acted upon without the appropriateness of that information having regard to those factors. You should assess whether or not the information contained herein is appropriate to your individual financial circumstances and goals before making an investment decision or seek the help the of a licensed financial adviser. Performance is historical; performance may vary; past performance is not necessarily indicative of future performance. Any prices, quotes or statistics included have been obtained from sources deemed to be reliable, but we do not guarantee their accuracy or completeness.